Options for operating efficiently and sustainably within forest water licence rules

Lead researcher: Professor Jeff Connor

The Project

The report on economics value of water accounting and licencing options industry can propose. Develop spreadsheet application for forest industry to evaluate economics of responses to new water licencing requirements.

Uniquely, plantation managers have the opportunity to manage their forest and licenced water assets for economic and financial advantage and develop methods to efficiently operate within forest water licence regulations.

The objective of the project is to enhance the Lower LImestone Coast forest industry's capacity to understand options to effectively and profitably adjust to forest water licencing requirements, specifically:

- Interactive sessions between industry and researchers to develop shared understanding. Validate case study details, water licencing understanding, technical and financial data.

- Develop spreadsheet style financial analysis and case study, explore early results in interactive session to odify in light of industry insights, revise and fianlise including assessment of alternate water licence variations.

- Deliver a report for industry to present to the water regulator and for their own consideration.

The project evaluated financial and profit implications of alternative strategies to manage forest assets within water licence requirements including options to buy/sell/lease water rights when required or are excess to requirements.

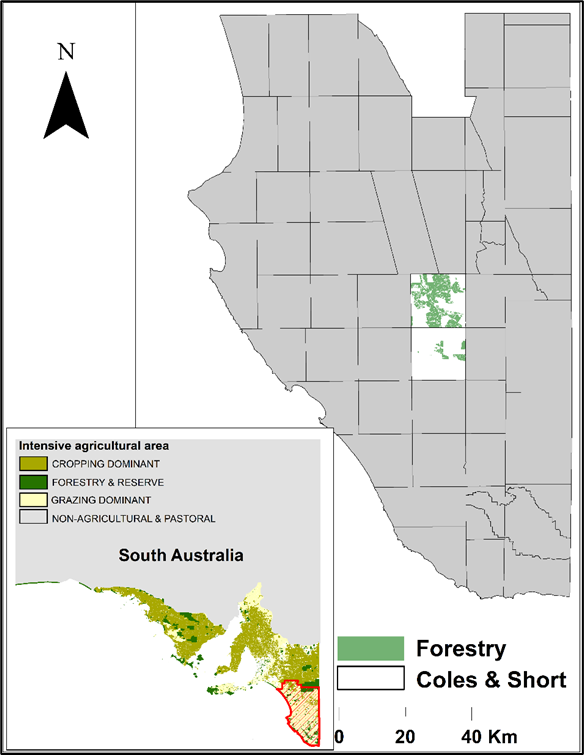

The Lower Limestone Coast study area. The Coles and Short Water Management Zones and forest inventory

Our Research Approach

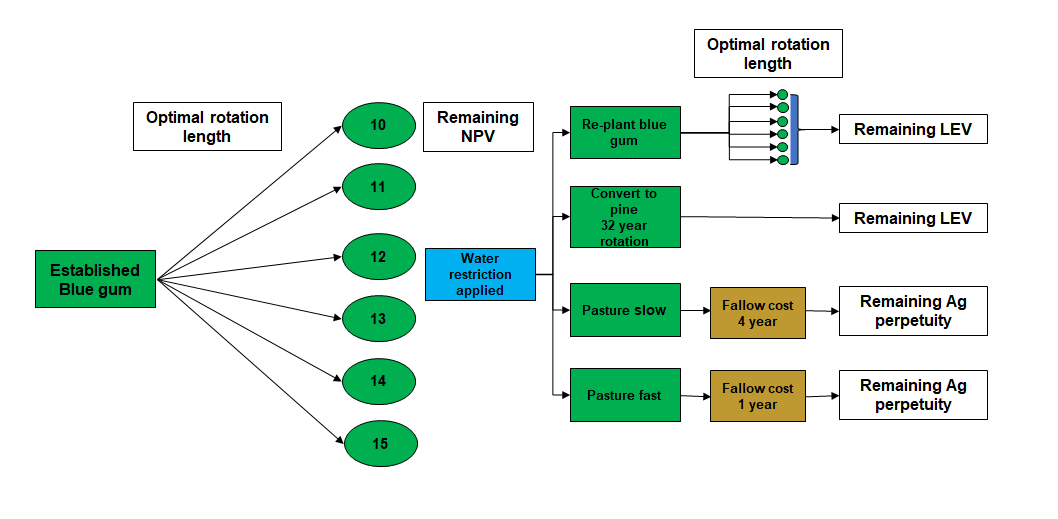

Hardwood industry scenarios agreed to represent viable options for a forestry company with hardwood holdings in the WMAs of Coles include:

- A business as usual scenario (BAU) assumes no cuts to water allocation and that all land held by the forest copanies remain in blue gum production. Rotation length is a choice variable in this scenario and a profit maximisation objective identifies economically optial rotation length for standing inventory and for current and subsequent rotations.

- A water restrictions scenario (WR). Water allocation reductions become binding when standing timber is harvested. There are 51 percent less allocations than would be required to replant all hardwood areas standing at present. Rotation length and locations to replant hardwoods to maximise profit are the decision variables. It is assumed that land not replanted to hardwoods is converted to non-irregated pasture and leased for an annual rent.

- A fast or slow conversion scenario (FS). The FS scenario is the same as the WR scenario except that fast or slow to agriculture is possible with faster conversion at higher site renovation cost.

- A sell water scenario (SW). Teh SW is the same as scenario to FS but the additonal option to sell water allocation is introduced. This is possible when harvesting hardwoods and converting land to dryland agriculture reduces water use below water allocation.

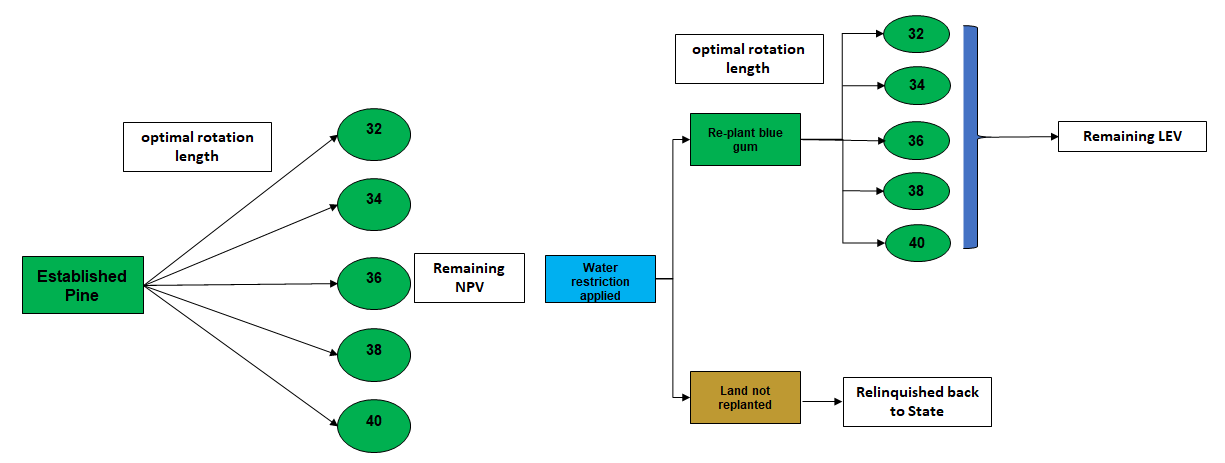

Pine industry scenarios agreed upon represent viable options for a forestry company with pine holdings in the Short WMA. Short was chosen becuase the larger pine inventory and large potential additional water constraint. The scenarios include:

- A business as usual scenario (BAU) assumes not cuts to water allocation and that all land held by the forest companies remains in pine production. The scenario calculates the returns from continued 32-year rotations.

- The second scenario assesses rotation length as a choice variable and a profit maximisation objective identifies economically optimal rotation length for standing inventory and for subsequent rotations.

- In a water restriction secenario (WR) water allocation reductions becoming binding when standing timber is harvested. There are 44 percent less allocations than would be required to replant all pine areas standing at present. Rotation length and locations to replant softwood to maximise profit are the decision variables. It is assumed that land not replanted to pines provides no more benefit to the pine industry. Unlike for the hardwood industry, conversion to non-irrigated pasture and earning the return fro this enterprise is not possible under the lease conditions that most of the pine industry operates. The aim of this scenario is to understand pine forest sector econoic impacts of proposed reductions to water availability.

Our Findings

The Lower Limestone Coast Water Allocation Plan (LLC WAP) was implemented to address the declining condition of ground water resources in the South East of South Australia. As part of the LLC WAP limitations on resource access for ground water using industries have been implemented to ensure long term water resource condition is maintained and to protect ground water dependent ecosystems. Commercial forestry is a significant land use in the area and has been identified as a major user of water resources in the region. The WAP requires that commercial forestry plantations now need to account for

their water use by holding forestry water licenses with sufficient allocation to support forestry activities.

The aim of this research was firstly to explore the likely economic consequences further water allocation reductions would have on forestry operations in the LLC and; with industry partners develop adaptation strategies and explore their economic basis.

The results indicate that for a hardwood plantation manager with assets in the WMA of Coles a 51 percent reduction in water allocation implemented after harvest of standing estates would result in a 13 percent reduction in NPV. This scenario assumes that land not replanted to hardwood would be converted to dryland agricultural production and leased.

The results showed that in all cases land should be converted to agriculture quickly, in this instance in one year, and back to full agricultural production as rapidly as possible.

The softwood industry scenarios were somewhat different in nature to the hardwood industry scenarios. The option to convert land to another land use is not considered in this modelling. Of interest to softwood industry partners was the option to extend rotation length, thereby delaying the implementation of any allocation cuts.

The results show that extending rotation length to 36 years would increase the NPV from the fixed rotation length scenario by approximately 3 percent. This comparison did not include a water restriction.

While the results presented in the final report show seemingly viable adaptation options for the forestry industry in response to the LLC WAP, they do not account for the effect on other factors such as the impact reduced timber volumes have on other variables.

The results are also contingent on the assumptions made regarding plantation ages, productivity and the costs and returns from forestry and agricultural enterprises.

What is the Future of R&D regarding Forest Water Licence Rules?

Whilst research reported on here had a very specific objective, this project and second on biosecurity offered the UniSA business school the opportunity to develop industry capacity to evaluate a large range of diverse issues with economic dimensions within the forestry industry. It is hoped that the capacity and relationships being developed through the NIFPI framework will be able to be further developed into the future and employed on other problems with economic dimensions facing the commercial forestry industry.

Our team

Researchers: Jeff Connor, Courtney Regan, Jim O'Hehir, Will McKay, Sayed Iftekhar (Griffith University).

Collaborators: Australian Bluegum Plantations, Green Triangle Forest Products, OneFortyOne Plantations Ltd, PF Olsen, SFM Asset Management.

Contact information

Dr Jim O’Hehir

General Manager: Forest Research Mount Gambier

Ph: +61 8 830 28997

E: Jim.O'Hehir@unisa.edu.au

Michele Cranage

Administrative Officer

Ph: +61 8 830 28902

E: Michele.Cranage@unisa.edu.au